The segmentation of the multi-layer blown films market across material type, manufacturing process, and end-user industry is genuinely useful for strategic analysis because the decisions at each segmentation level are interdependent in commercially significant ways. A food manufacturer specifying packaging for a fresh meat product needs oxygen barrier performance that determines whether polyamide or polyvinylidene chloride is included in the film structure. That material choice constrains which manufacturing process can efficiently produce the required film structure. And the production volume of the application determines which process economics are most appropriate. Reading these interdependencies is what makes segment analysis in this market actionable.

The Multi-Layer Blown Films Market Share is distributed across polypropylene, polyethylene, polyamide, polyvinylidene chloride, polystyrene, and nylon material categories; blown film extrusion, co-extrusion lamination, cast film extrusion, and co-extrusion coating process types; and electronics, food and beverages, pharmaceuticals, consumer goods, and other end-user categories. The market is expected to register a positive CAGR of 4% from 2025 to 2031 as per the full report.

Why is polyethylene typically the largest material segment in the multi-layer blown films market?

Polyethylene's dominance reflects its versatility across the widest range of multi-layer film applications, its compatibility with virtually all co-extrusion partners across the polymer spectrum, its cost competitiveness among all polymer options, and its suitability for the heat sealing processes that flexible packaging requires. Linear low-density and low-density polyethylene grades provide the sealing, flexibility, and puncture resistance properties that form the outer layers of most multi-layer blown film structures across food, consumer goods, and industrial applications, making polyethylene present in the vast majority of all multi-layer blown film products regardless of which other barrier or structural polymers are included.

Download Sample PDF @ https://www.theinsightpartners.com/sample/TIPRE00023355

Key Market Players

- Ultimate Flexipack Limited

- Optimum Plastics

- Girish Polychem Industries

- HOSOKAWA ALPINE Aktiengesellschaft

- ISO POLY FILMS, INC.

- Danafilms Corp.

- Borealis AG

- SIVA GROUP

- Raven Engineered Films

- Division Balcan Plastic

Segments Covered

By Material

- Polypropylene

- Polyethylene

- Polyamide

- Polyvinylidene Chloride

- Polystyrene

- Nylon

By Process

- Blown Film Extrusion

- Co-Extrusion Lamination

- Cast Film Extrusion

- Co-Extrusion Coating

By End User

- Electronics

- Food and Beverages

- Pharmaceuticals

- Consumer Goods

- Others

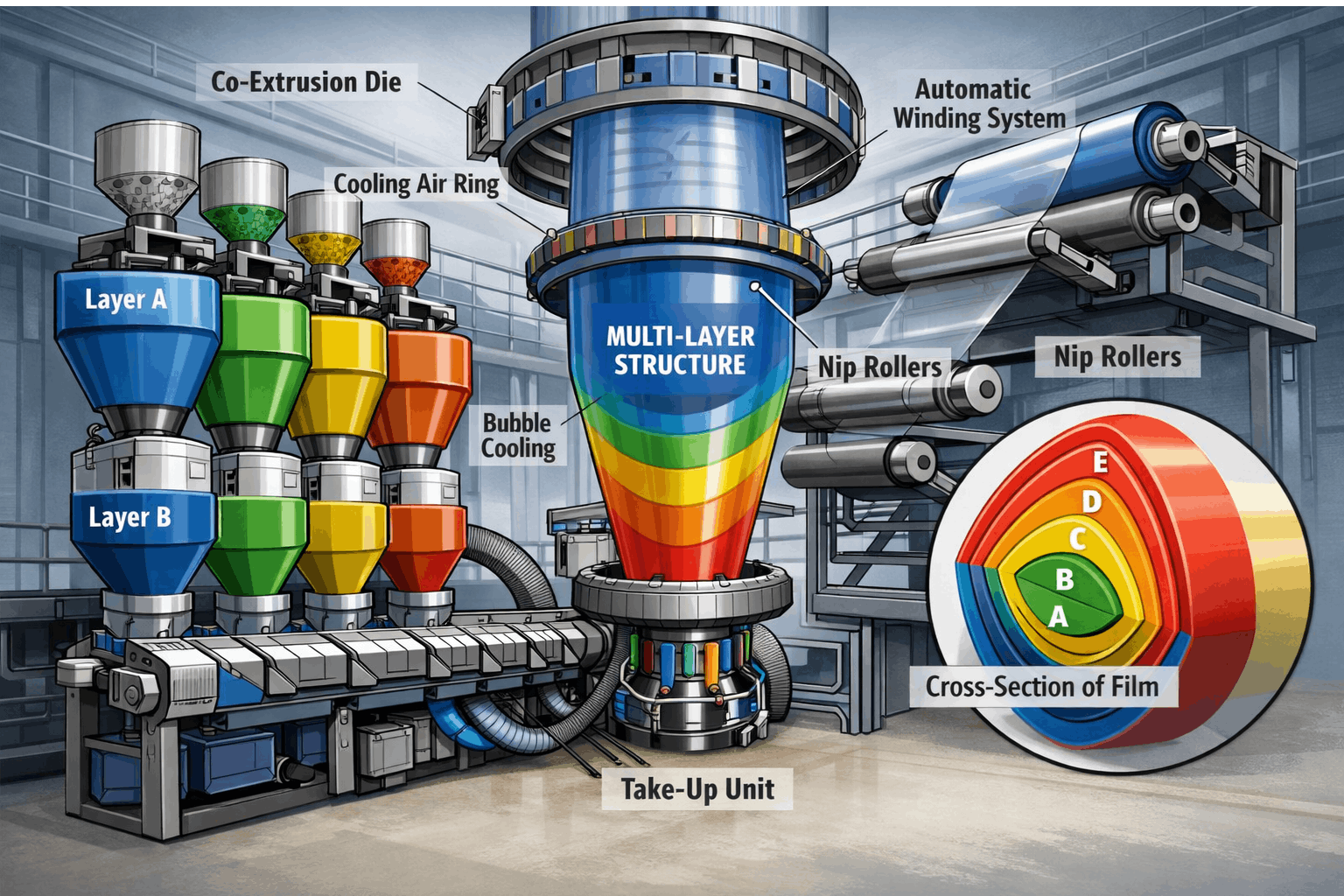

Process Segmentation: Co-Extrusion as the Technology of Choice

Co-extrusion processes, encompassing both blown film co-extrusion and co-extrusion coating, represent the commercially dominant manufacturing approach for multi-layer blown films because they produce the defined layer structure in a single pass operation that delivers better inter-layer adhesion, more consistent layer thickness distribution, and more competitive production economics than lamination or coating processes applied to pre-formed films. The ability to design and adjust layer compositions and thicknesses in a single production step gives co-extrusion lines the flexibility to serve diverse customer specifications efficiently, making co-extrusion investment the preferred capacity addition strategy among leading film producers.

End-User Segment Dynamics

Food and beverages drives the largest end-user demand volume across all five geographic regions covered by the report. Pharmaceuticals represents the highest specification and highest unit value end-use category, where film properties including moisture barrier, oxygen transmission rate, and chemical compatibility must meet regulatory standards that commodity film grades cannot satisfy. Consumer goods and electronics contribute consistent incremental demand across protective packaging and anti-static film applications respectively. The complexity of multi-layer film manufacturing compared to monolayer alternatives represents the primary restraint on market growth, as smaller converters and producers in cost-sensitive markets may resist the capital investment that advanced co-extrusion equipment requires.

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us

The Insight Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com

Also Available In : Korean | German | Japanese | French | Chinese | Italian | Spanish