The global Body-Worn Camera Market Size has expanded into a multi-billion-dollar industry and continues to grow at a remarkable rate. This substantial market valuation is a direct reflection of the massive global investment by law enforcement agencies and other public safety organizations into this transformative technology. The market size is a comprehensive measure that encompasses not just the initial, one-time sales of the physical camera hardware, but also, and more importantly, the recurring and long-term revenue generated from associated services. This includes the massive and growing spending on cloud-based data storage, subscriptions to digital evidence management software (DEMS), and contracts for ongoing technical support and maintenance. The market's strong and sustained growth trajectory is a clear indicator that body-worn cameras have moved from being a pilot project or a niche item to being considered a standard and essential piece of equipment for modern law enforcement worldwide.

A breakdown of the market size by component clearly illustrates the industry's business model. The hardware segment, which includes the body-worn cameras themselves and the docking stations, accounts for a significant portion of the initial revenue when an agency first deploys a program. However, the software and services segment is the largest and most valuable part of the market, and it is where the long-term, recurring revenue is generated. The immense volume of high-definition video generated by a police department requires a massive amount of secure cloud storage, and the fees for this storage represent a huge and growing component of the market size. Subscriptions to the sophisticated DEMS platforms, which provide the tools for managing, redacting, and sharing this evidence, are another major source of recurring revenue. This shift from a hardware-centric to a software-and-service-centric model is a key characteristic of the market, creating a "sticky" customer base and a highly predictable revenue stream for the leading vendors.

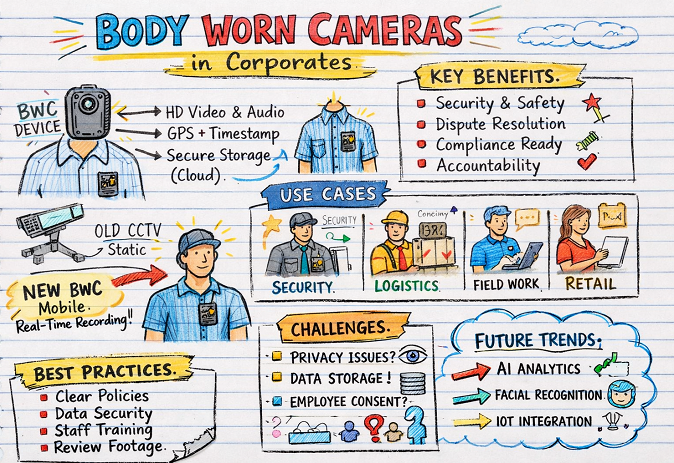

When analyzed by end-user, the law enforcement segment is, by a very wide margin, the largest and most dominant contributor to the market size. Police departments in cities large and small around the world are the primary customers, driven by the powerful push for accountability and transparency. This segment alone accounts for the vast majority of current market spending. However, other segments are emerging and growing rapidly, contributing to the market's expansion. The corrections segment (prisons and jails) is a significant and growing market, where BWCs are used to enhance the safety of both officers and inmates. The private security industry is also a fast-growing adopter, equipping guards at shopping malls, corporate campuses, and events with cameras. Other nascent but promising end-user segments include emergency medical services, transportation authorities, and even sectors like retail and hospitality, where cameras can be used to document incidents and improve staff safety.

Geographically, the body-worn camera market size is currently dominated by North America, with the United States being the single largest market in the world. This is a direct result of the intense public and political focus on police reform in the U.S., which has led to widespread adoption and significant federal funding to support BWC programs at the state and local levels. Europe, particularly the United Kingdom, is another major and mature market with a long history of using CCTV and a strong focus on evidence-based policing. The Asia-Pacific region is projected to be the fastest-growing market in the coming years. As public safety agencies in countries across this region seek to modernize their operations and respond to their own societal demands for greater transparency, there is a huge opportunity for market expansion. The continued global focus on police-community relations, coupled with ongoing technological advancements, will ensure that the global market size continues its strong upward trajectory.

Explore More Like This in Our Regional Reports: